All Categories

Featured

Table of Contents

[/video]

. They are just getting begun. They do, um, this for their deposit. What we do is we will certainly structure a time period that functions for you. If you're taking a lending and you want to settle it on a specific time period, you will work with you to come up with what time duration do you desire to settle it on? And after that that financing settlement will just compose out of your bank account when a month or whatever regularity you desire it to be set on.

That's paying you even more than your costs. And if you're a, if you're in advance, then you simply take a section of that and use that to pay back the financing.

It just works out extremely well for buy and hold investors. Okay. There's no, , there's no halt on buy and hold. A lot of people do the ruptured approach with this. I have people that do submissions. The syndications usually have a 3 to 7 year hold period, depending upon what it is that they're doing.

And afterwards you have an exit where you obtain a huge equity, numerous in some cases as high as like 1.7, 5 or 2 X equity, multiple. And after that they pay back whatever. When they exit a couple of years later, simply let the lending rate of interest rate accrue over that time, or they pay it back as things of cash money circulations during the preliminary financing duration, due to the fact that they can certainly cashflow simply the rates of interest.

It functions for buy and hold. Let me just ask one even more inquiry, just to get a little bit deeper right into the concern of long-term buy and hold utilizing this technique, utilizing this bundle, this policy, due to the fact that my mind is obsessed on buy and hold lasting.

Nevertheless, I require a plan don't I to amortize or pay that off over a particular time period. Whether I wish to pay it off over 5 years or 20 years, I do need to cover the passion, however after that also apply extra principle to pay down that home loan.

Infinite Banking Spreadsheet

Yeah, you certainly wish to do that Marco (your own bank). And that is why we can do organized settlement. Okay. So I can have a means for you to state, you understand what, I wish to put $800 a month in the direction of paying that lending off and or whatever quantity that fits wherefore your strategy is.

Every month it gets paid back. And that means you can then obtain more completely dry powder again, to go out and wash and duplicate and do it once again.

I wasn't able to obtain right into every subtlety to information, yet there's a minimum amount that you can contribute and a maximum. You can place, allow's simply state up to a hundred thousand and as low as 50,000. So there's this big window of just how much you can put in annually to your policy.

They just allow you put in so much. Now what it is right currently is 25% of your earnings is your regular payment cap. You can obtain, if you are making 200,000 a year, simply as a round number example, you can place in up to $50,000 a year, $400,000 a year revenue, you would a whole lot be allowed to put in a hundred thousand dollars a year.

And I generally do that. Um, it's, it's a means to simply do a lump sum cash contribution the initial year, if you're setting on cash in an interest-bearing account that you wish to move right into this, all of that added amount is generally offered after thirty day. So that's why I do it hat way.

Be Your Own Bank Life Insurance

And I intend to just deal with that actual quick, due to the fact that the solution to that is that in order for it to still be thought about life insurance by the federal government, okay, you have to a minimum of make 7 payments. So it's this mech screening policies and they ensure you're not trying to make a financial investment out of life insurance policy.

And I generally extend that and go, you recognize, allow's play it safe and prepare for eight. And the various other thing is, do I need to put in the maximum that is created or just the minimum, of training course, you're only responsible for the minimum. And afterwards the other thing that people ask me is what if I'm 2 or 3 years in, and I can't make a payment, I require to skip an entire year.

And after that after you get back on your feet or a financial investment cells, then you can go back and make up with a catch-up contribution, the quantity that you were brief the prior year. There's a great deal of adaptability to this. And I simply desire individuals to realize if they're worried about a commitment, due to the fact that I assume it's a long-lasting commitment.

And the means I structured is to provide you the maximum adaptability. Certain. So my website is I N F O. And that's where you go to get details concerning this. So I have the ability for you individuals that are listening to this program. You just go there to that site, placed in your name and email and you will certainly obtain accessibility to an amazing video training collection that I have actually spent years perfecting and getting it all limited to make sure that it's not losing your time.

The Infinite Banking Concept

So I believe you can see like the first six really stuffed video clips for in regarding 45 mins. Which will give you a great understanding of what it is that this is all around. And after that right there on that particular page, if you wish to call me, there's a way to just book a time to chat and I can review and reveal you what your personal capacity to do.

Yes. I understand podcasts and numbers do not work out with each other, but I do have to offer some kind of some sort of simply, that's why I always use round numbers to make it to where it's easy ideas. But I, you know, I understand that that is, that is tough.

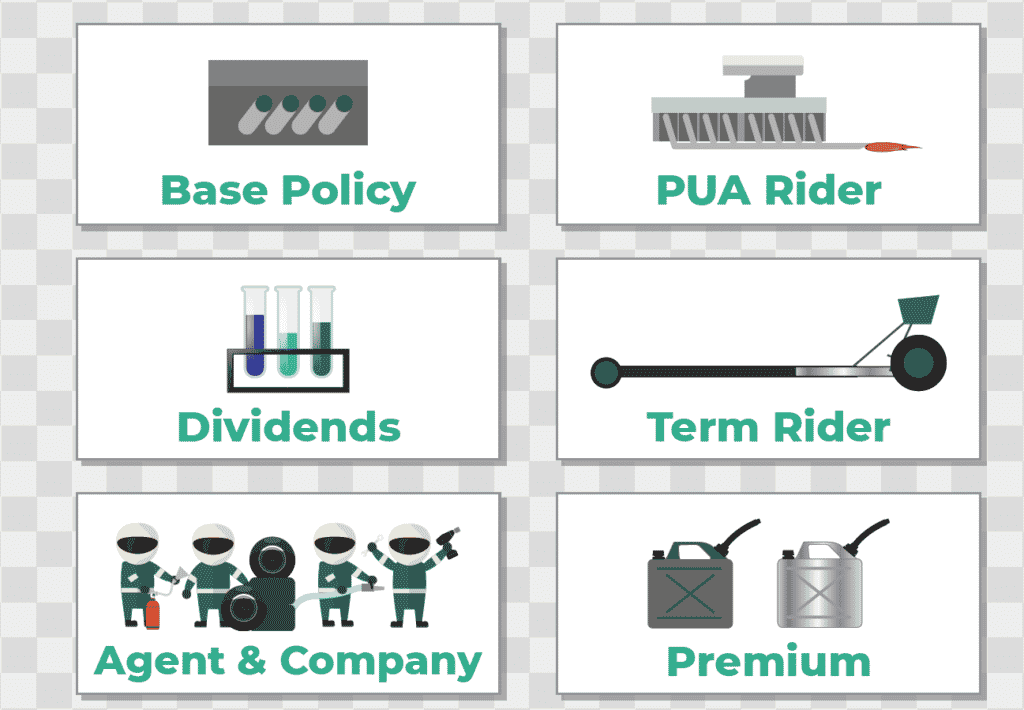

Is it actually true that you can become your own bank? Yes, it's real. And yes lots of people do not recognize it's a thing. In the money world, we call this strategy limitless financial. Unlimited financial refers to the procedure of becoming your very own lender. The functional approach at play? Leveraging a really particular type of retired life cost savings account, and establishing it up to be used while you are still active.

On one of the most basic level of recognizing this, your cash is being taken into an account that grows at a much higher price than a normal savings account at a standard bank. This account is equally as fluid as an interest-bearing account; tax-free; and is not place right into risky investments where you can lose cash.

By 'no threat' we mean that your money never ever goes 'in reverse' as in it will just remain to grow. Currently, this is the kicker. With this account you are able to accessibility tax totally free "financings", which are taken against your very own money. You can after that utilize these fundings in order to money your acquisitions or endeavors as opposed to needing to make use of a standard bank to accessibility financings, or tackling the passion that features them.

Profile For Be Your Own Bank

Which they use to take loans from (while still expanding interest), in order to offer various other individuals individual car loans/ home mortgages/ credit cards, to likewise then charge them rate of interest on top of all of it. This suggests the bank is generating income in rather a couple of ways. 1) Their limitless checking account grows continuous compound rate of interest through powerful dividends through certain companies (extra on this in future short articles.)2) They take your money to pay their limitless financial institution when they take fundings out of it.

If any of that went over your head, don't stress. And when you take out a financing, every payment you make back on the financing can go right back to the principal in your own account.

However, regardless of what occurs you constantly obtain guaranteed 4%. This implies you're getting a strong growth a whole lot a lot more effective than a standard financial savings account, and without having to tackle market threat. What this means is that your account constantly increases and never goes down. The reason that this is so wonderful is due to the fact that you will be contributing a constant amount of cash every month right into an account with no risk.

{kind=link}

Latest Posts

Be Your Own Bank Through Bitcoin Self-custody

Infinite Banking Life Insurance

Infinite Banking System